SVB vs Transfer Pricing – In international trade, businesses often face two major valuation challenges—Customs Valuation and Transfer Pricing. Though both deal with the value of imported goods, they arise under two different laws: the Customs Act and the Income Tax Act. Yet, they intersect in surprising ways.

At Rajendra Law Office LLP, we have seen many companies struggle when the Special Valuation Branch (SVB) of Customs and the Transfer Pricing Officer (TPO) from the Income Tax Department examine the same transaction with different perspectives. This intersection can create confusion, double scrutiny, and compliance risks.

SVB vs Transfer Pricing: How Customs and Income Tax Intersect in Valuation of Imports: Rajendra Law Office LLP

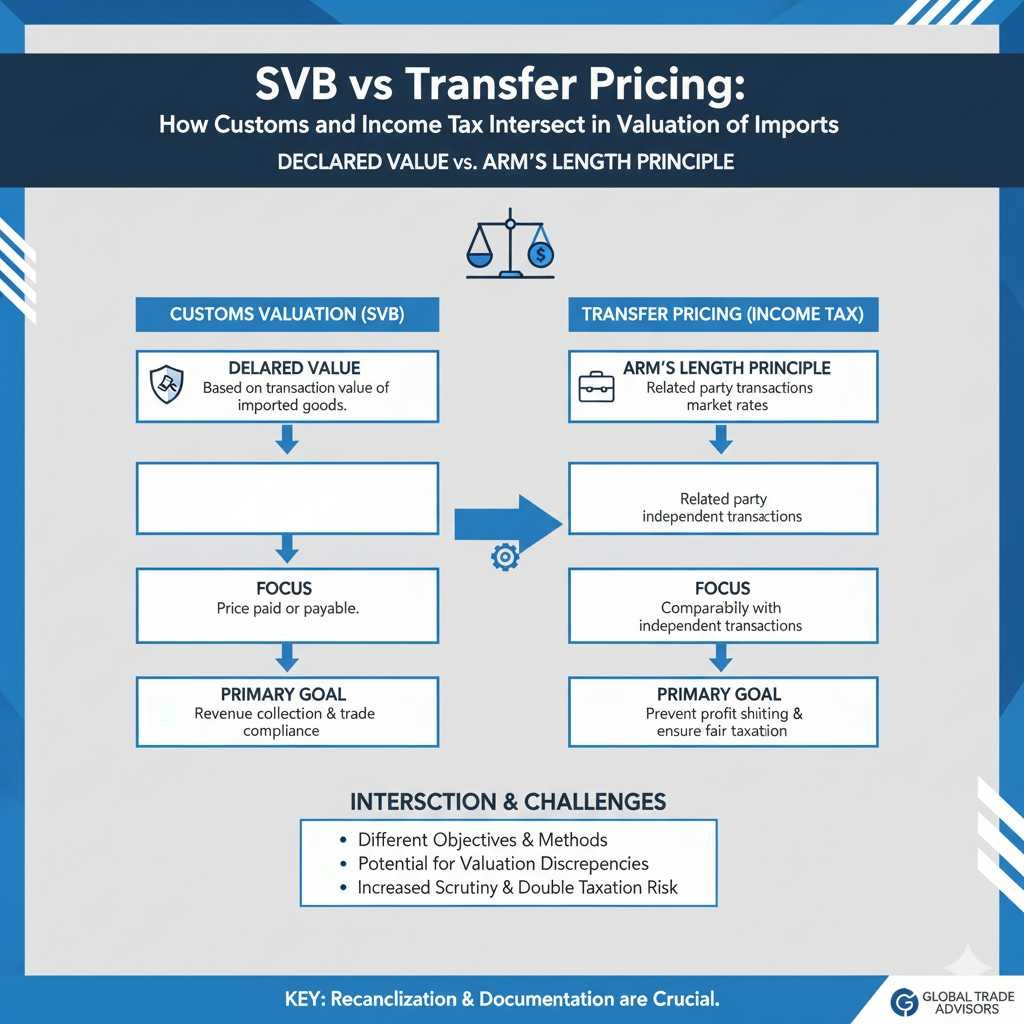

Understanding SVB: The Customs Perspective

The Special Valuation Branch (SVB) is a division under the Indian Customs Department that deals with valuation of goods imported between related parties. When an Indian company imports from its foreign parent, subsidiary, or affiliate, Customs wants to ensure that the declared price is not manipulated to evade duty.

The SVB investigates whether the relationship between importer and supplier has influenced the price. It examines agreements, invoices, pricing policies, and financial details. After review, it either accepts the declared value or directs an upward revision.

In short, SVB ensures that Customs duty is calculated on a fair and arm’s length transaction value.

Understanding Transfer Pricing: The Income Tax Perspective

On the other side, the Transfer Pricing mechanism under the Income Tax Act, 1961, ensures that international transactions between related parties are priced at arm’s length—the same price that unrelated parties would pay under similar conditions.

Here, the focus is on profits and tax revenue, not import duty. The Transfer Pricing Officer (TPO) examines whether the price charged in international transactions affects the taxable income of the Indian entity.

So, while SVB protects customs revenue, Transfer Pricing protects income tax revenue. Both systems try to ensure fairness, but from opposite directions.

Why SVB and Transfer Pricing Often Overlap

For multinational businesses, import transactions with group companies fall under the lens of both Customs and Income Tax authorities. Both departments examine related party transactions, pricing, and arm’s length value, which creates a natural overlap.

However, their objectives differ:

- Customs wants to ensure the import price is not undervalued to avoid duty.

- Income Tax wants to ensure the price is not overvalued to shift profits out of India.

Ironically, the same transaction could appear underpriced to one department and overpriced to another. This leads to conflicting adjustments—and that’s where expert legal handling becomes crucial.

Key Differences Between SVB and Transfer Pricing

| Aspect | SVB (Customs) | Transfer Pricing (Income Tax) |

|---|---|---|

| Governing Law | Customs Act, 1962 | Income Tax Act, 1961 |

| Authority | Special Valuation Branch (Customs) | Transfer Pricing Officer (Income Tax) |

| Objective | Prevent undervaluation of imports | Prevent profit shifting and tax evasion |

| Focus | Import transaction value | Cross-border pricing and profits |

| Method | Customs Valuation Rules (CVA) | Arm’s Length Price (ALP) Methods |

| Outcome | Impacts Customs Duty | Impacts Income Tax Liability |

Even though their focus is different, both rely on comparables, documentation, and independent valuation methods.

How Customs Determines Related Party Valuation

Under Rule 2(2) of the Customs Valuation Rules, 2007, two parties are considered “related” if one controls, owns, or influences the other. When such a relationship exists, Customs asks the importer to file a SVB Questionnaire along with agreements, pricing policy, and transfer pricing documents.

The SVB then analyses:

- The nature of the relationship.

- The price-setting mechanism.

- The terms of supply and payment.

- Comparables from unrelated transactions.

If the declared value is found influenced by the relationship, Customs can enhance the assessable value for duty calculation.

Thus, SVB aims to make sure that imports reflect true commercial value, not a manipulated one.

How Transfer Pricing Determines Arm’s Length Value

Transfer pricing uses methods prescribed under Section 92C of the Income Tax Act, such as:

- Comparable Uncontrolled Price (CUP) Method,

- Resale Price Method,

- Cost Plus Method,

- Transactional Net Margin Method (TNMM), or

- Profit Split Method.

The taxpayer must maintain detailed Transfer Pricing Documentation to justify that the international transaction is at arm’s length.

If the TPO finds that the price paid for imports is too high or too low compared to market rates, they can adjust the taxable income. This directly affects the company’s tax liability.

The Intersection: When SVB and TPO Look at the Same Data

The most challenging situation arises when the SVB and TPO both examine the same import transaction but reach different conclusions.

For example:

- The SVB may say the declared import price is too low (undervalued) and increase the assessable value for Customs Duty.

- The TPO may say the same import price is too high (overvalued) and increase the taxable income for Income Tax.

Both adjustments together can result in double taxation—higher customs duty and higher income tax—on the same transaction.

At Rajendra Law Office LLP, we often handle such cross-departmental disputes by presenting coordinated legal documentation that satisfies both authorities without harming the client’s position.

Common Challenges Faced by Importers

Businesses dealing with related-party imports often face:

- Dual scrutiny by Customs and Income Tax.

- Delay in clearance due to pending SVB investigations.

- Inconsistent valuation standards between departments.

- Demand notices or penalties for alleged misdeclaration.

- Difficulty reconciling ALP and assessable value.

- Burden of maintaining extensive documentation in both regimes.

Without legal coordination, such issues can lead to financial loss and reputational risk.

Legal Remedies and Best Practices

To avoid or resolve SVB and Transfer Pricing conflicts, businesses should follow structured legal and procedural steps:

1. Prepare Harmonized Documentation

Ensure that Customs valuation reports and Transfer Pricing documentation align in explaining how prices were determined. Contradictions between them can invite suspicion.

2. File SVB Questionnaire Carefully

Provide detailed answers supported by inter-company agreements, cost sheets, and comparable prices. A clear, transparent approach often helps obtain SVB approval faster.

3. Maintain Consistent Valuation Policies

The pricing mechanism mentioned in your transfer pricing study should match what’s declared to Customs.

4. Seek Advance Rulings or Clarifications

In complex cases, you can apply for an Advance Ruling under Customs or a Transfer Pricing Advance Pricing Agreement (APA) under Income Tax. These bring certainty and reduce future disputes.

5. Engage Legal Experts Early

Professional representation ensures proper filing, argument, and reconciliation before both authorities. At Rajendra Law Office LLP, our lawyers handle joint documentation reviews, representations, and appeals for clients facing dual inquiries.

The Role of Legal Experts: Bridging the Gap

When Customs and Income Tax operate in silos, businesses face duplication of effort and risk of double assessment. Skilled legal advisors act as bridges between departments.

Our firm’s approach involves:

- Aligning valuation positions under both Acts.

- Representing clients during SVB hearings and TPO proceedings.

- Drafting replies that highlight consistency in pricing logic.

- Coordinating with chartered accountants and tax consultants to present a unified defense.

- Negotiating settlements or appeals where necessary.

By ensuring harmony in documentation and reasoning, we help clients achieve compliance without paying twice for the same transaction.

Recent Trends and Government Coordination

In recent years, the Indian government has recognized the need for greater alignment between Customs and Income Tax departments. Initiatives are being discussed for data sharing between SVB and TPO to reduce duplication.

The Model Customs Valuation Manual and CBDT transfer pricing guidelines both emphasize consistency in applying the arm’s length principle.

Still, practical challenges persist because the laws serve different fiscal objectives. Businesses must therefore proactively align their internal systems.

Practical Example: A Case Study

Consider a Chennai-based manufacturing subsidiary importing raw materials from its parent company in Germany. The declared price per unit is ₹1,000.

- Customs (SVB) suspects undervaluation and revises the assessable value to ₹1,200 for duty purposes.

- The Income Tax TPO, during assessment, finds the price too high compared to local market rates and adjusts it down to ₹900 for tax computation.

The result: the company pays higher customs duty and higher income tax on opposite assumptions.

Our legal team intervenes by preparing a consolidated valuation justification, supported by global comparables and cost data. After hearings and submissions, both authorities accept the adjusted figure of ₹1,050, bringing consistency and saving the client from double exposure.

This example shows how coordinated legal strategy prevents contradictory outcomes.

Key Takeaways for Businesses

- Always identify if your supplier is a related party under Customs and Income Tax laws.

- File complete SVB documentation at the time of import registration.

- Maintain consistent pricing explanation across all departments.

- Update your Transfer Pricing study annually with accurate import data.

- Use professional legal assistance for any valuation dispute or notice.

- Consider Advance Pricing Agreements (APAs) to ensure long-term predictability.

- Keep all agreements, invoices, and cost sheets ready for inspection.

- Avoid conflicting statements during audits or investigations.

- Cooperate with both authorities through transparent communication.

- Seek timely legal advice to prevent escalation into litigation.

How Rajendra Law Office LLP Assists Clients

At Rajendra Law Office LLP, we specialize in handling complex cross-border valuation issues involving Customs and Income Tax departments. Our services include:

- Drafting and filing SVB applications and questionnaires,

- Preparing and reviewing Transfer Pricing documentation,

- Representing clients before Customs, TPO, and appellate authorities,

- Conducting joint reconciliation of valuation records,

- Advising on Advance Pricing Agreements and rulings,

- Providing legal opinions on valuation consistency,

- Managing dispute resolution through negotiation or appeal.

With decades of experience in both trade and tax law, our lawyers ensure that clients maintain compliance while minimizing financial exposure.

Frequently Asked Questions

The Special Valuation Branch (SVB) of Indian Customs examines import transactions between related parties, such as parent and subsidiary companies. Its role is to determine whether the declared import price has been influenced by the relationship. If the price is found undervalued, Customs may adjust the assessable value to ensure fair duty payment. SVB helps maintain transparency and prevents customs duty evasion.

Transfer Pricing, governed by the Income Tax Act, ensures that international transactions between associated enterprises are priced at arm’s length. Unlike SVB, which focuses on preventing undervaluation for customs purposes, Transfer Pricing ensures that profits are not shifted to avoid tax. Essentially, SVB protects customs revenue, while Transfer Pricing protects income tax revenue—two sides of the same valuation coin.

Yes, both authorities can examine the same related-party import transaction. However, their objectives differ—SVB focuses on customs duty, while Transfer Pricing focuses on taxable income. Often, their findings may conflict. Proper legal coordination ensures that both assessments remain consistent and prevent double taxation.

Businesses often face dual scrutiny, document mismatches, delays in import clearance, and conflicting valuation interpretations. Maintaining consistent documentation and seeking expert legal help ensures smoother proceedings and fewer disputes.

Rajendra Law Office LLP offers end-to-end legal assistance, including SVB filings, Transfer Pricing documentation, representation before Customs and Income Tax authorities, and reconciliation of valuation positions. The firm ensures legal compliance, consistent reporting, and protection against double taxation.

Conclusion: Bridging Compliance Through Legal Clarity

The intersection of SVB and Transfer Pricing is a complex field where two laws meet but often conflict. Without proper coordination, businesses may end up paying double—once in customs duty and again in income tax.

However, with the right legal guidance, companies can achieve harmonized valuation, regulatory confidence, and peace of mind.

Read More

- GST Advance Ruling and Cross-Border Transactions: What Importers and Exporters Must Know

- How to Report Income Tax Violations in India | A Legal Guide

- SVB in Indian Customs Explained: Why Businesses with Foreign Affiliates Should Stay Compliant

- Covering All Grounds: Exploring the Diversity of Criminal Cases Handled

- Public Interest Litigation (PIL): Insights from Supreme Court Practice

- Central Board of Indirect Taxes and Customs (CBIC) – Tax Information page on customs valuation and related Acts/Rules

- Income Tax Department – Tax Payers Information Booklets page (contains booklets on Transfer Pricing as part of Chapter X of the Income-tax Act)